Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

With health care costs rising 18 per cent annually, having a high cover has become a necessity

The average premium per policy in 2003-04 was Rs 4,166 and the number of people insured per policy was four. By 2010-11, the premium per policy had increased to Rs 14,120 and the number of people insured per policy was six.

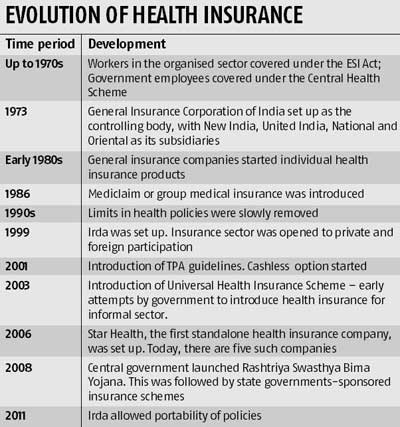

In 2006, the first standalone company was set up, Star Health Insurance. There are now five such companies. They are Max Bupa Health Insurance, Religare Health Insurance, Apollo Munich, Cygna TTK and Star Health.

In 2008, the central government launched the Rashtriya Swasthya Bima Yojana a social assistance scheme for below the poverty line families. Subsequently, Andhra Pradesh, Tamil Nadu and Maharashtra started state-sponsored insurance schemes. These helped widen the reach of health insurance.

Towards the end of 2009-10, companies started introducing innovations like covers for maternity and wellness treatments. Today, there are covers for pre-existing illness (albeit at a higher premium), day-care procedures where no hospitalisation is required, family critical illnesses and products with covers as large as Rs 50 lakh to Rs 1 crore.

An important step by Irda was the definition of pre-existing illness which made coverage of these after a maximum of four years a standard procedure. Allowing of portability of policies, the option to transfer to another company without any disruption in the waiting period, was another important feature, introduced in 2011.

Segar Sampathkumar, general manager, New India Assurance says the health insurance sector saw an annual growth of over 35 per cent in gross premiums between 2001-02 and 2013-14. "Although there was a slight tapering in the last two years, more and more hospitalisation will be funded by insurance as penetration improves," he says.

Although corporate health care does offer people better access to medical treatment, there remains the issue of whether it could push up costs, with over-investigation by doctors becoming as common as it has in the US. More to the point, perhaps, most of this evolution in health insurance does little to improve the average Indian’s access to health care.

Follow us on our social media channels:

Copyright © 2026 Design and developed by Fintso. All Rights Reserved

Industry News

Industry News